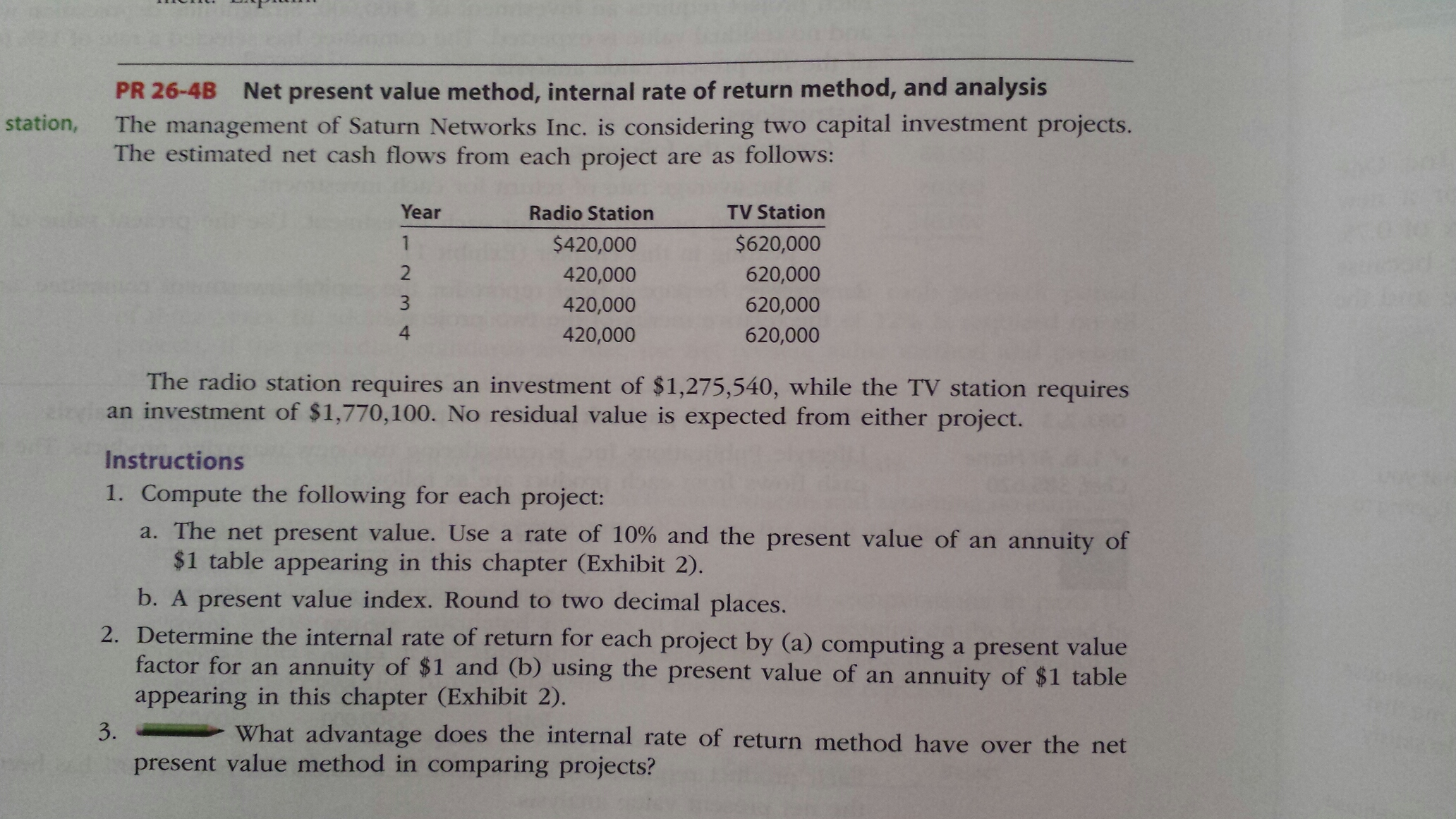

You essentially calculate the difference between the cost of a project, or its cash outflows, and the income generated by that project, or the cash inflows. NPV is calculated by finding the present value of each cash flow for each period, including any initial cash outflow that occurs immediately. The discount rate used is self-selected as the required rate of return for the project. Once all discounted cash flows have been calculated, add all cash flows to arrive at the net present value. IRR is most helpful when comparing projects or investments or when finding the best discount rate proves elusive.

Which of these is most important for your financial advisor to have?

The discount rate typically represents the cost of capital or the required rate of return. IRR is usually more useful when you are comparing across multiple projects or investments, or in situations where it is difficult to determine the appropriate discount rate. NPV tends to be better for when cash flows may flip from positive to negative (or back again) over time, or when there are multiple discount rates. Recall that IRR is the discount rate or the interest needed for the project to break even given the initial investment. If market conditions change over the years, this project can have multiple IRRs.

Definition of NPV

Financial managers and business owners usually like performance measures expressed in percentages instead of dollars. As a result, they tend to prefer capital budgeting decisions expressed as a percentage, as with the internal rate of return (IRR), instead of in a dollar amount, as with invoice price wikipedia net present value (NPV). IRR may also be compared against prevailing rates of return in the securities market. If a firm can’t find any projects with an IRR greater than the returns that can be generated in the financial markets, then it may simply choose to invest money in the market.

Shortcomings of IRR

For instance, suppose a private equity firm anticipates an LBO investment to yield an 30% internal rate of return (IRR) if sold on the present date, which at first glance sounds great. Conceptually, the IRR can also be considered the rate of return, where the net present value (NPV) of the project or investment equals zero. Because the IRR in our example exceeds the discount rate (or required rate of return), the IRR rule says that management should invest in this project. After subtracting the initial investment, the net present value of the project is $545.09, suggesting this is a good investment at the current discount rate. Internal Rate of Return, or IRR, is the rate of return at which a project breaks even and is used by management to evaluate potential investments. To determine the crossover rate, where the NPVs of two projects are equal, you can use Excel’s Goal Seek function.

- Any project with an IRR that exceeds the RRR will likely be deemed profitable, although companies will not necessarily pursue a project on this basis alone.

- The NPV can be used to determine whether an investment such as a project, merger, or acquisition will add value to a company.

- Without modification, IRR does not account for changing discount rates, so it’s just not adequate for longer-term projects with periods of varying risk or changes in return expectations.

- Excel does all the necessary work for you, arriving at the discount rate you are seeking to find.

IRR vs. Return on Investment (ROI)

In almost all cases where a prize winner is given an option of a lump-sum payment versus payments over a long period of time, the lump-sum payment will be the better alternative. For example, a corporation will evaluate investing in a new plant versus extending an existing plant based on the IRR of each project. In such a case, each new capital project must produce an IRR that is higher than the company’s cost of capital. Once this hurdle is surpassed, the project with the highest IRR would be the wiser investment, all other things being equal (including risk).

How is the IRR calculated?

However, in a certain project, both the two criterion give contradictory results, i.e. one project is acceptable if we consider the NPV method, but at the same time, IRR method favors another project. The internal rate of return is the discount rate that would bring this project to breakeven, or $0 NPV. Here, CFt represents the cash flow at time t, while n is project duration, CO denotes cash outflow and CI signifies cash inflow. This calculation provides an IRR, indicating the annual growth rate of the investment over the three-year period.

Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. 11 Financial is a registered investment adviser located in Lufkin, Texas.

The NPV Profile illustrates a project’s NPV graphed as a function of various discount rates. The NPV values are graphed on the vertical or y-axis, while the discount rates are graphed on the horizontal or x-axis. It looks very much like the NPV equation, except that the discount rate is the IRR instead of \(r\), the required rate of return. In other words, it is the rate at which an investment breaks even in terms of NPV.

Companies and analysts may also look at the return on investment (ROI) when making capital budgeting decisions. ROI tells an investor about the total growth, start to finish, of the investment. The two numbers normally would be the same over the course of one year but won’t be the same for longer periods. Using IRR to obtain net present value is known as the discounted cash flow method of financial analysis.

The Excel XIRR function is preferable over the IRR function as it has more flexibility by not being restricted to annual periods. Under XIRR, daily compounding is assumed, and the effective annual rate is returned. But for the IRR function, the interest rate is returned assuming a stream of equally spaced cash flows. What if you don’t want to reinvest dividends, but need them as income when paid? And if dividends are not assumed to be reinvested, are they paid out or are they left in cash?